Introduction

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) stands as the backbone of international financial messaging, enabling secure and efficient communication between financial institutions across the globe. Established in 1973, SWIFT revolutionized cross-border transactions by providing a standardized and reliable network for exchanging financial messages, replacing the slower and less secure Telex system. This article delves into the intricate anatomy of the SWIFT system, tracing its historical origins and examining its unique ownership structure.

Anatomy of the SWIFT System

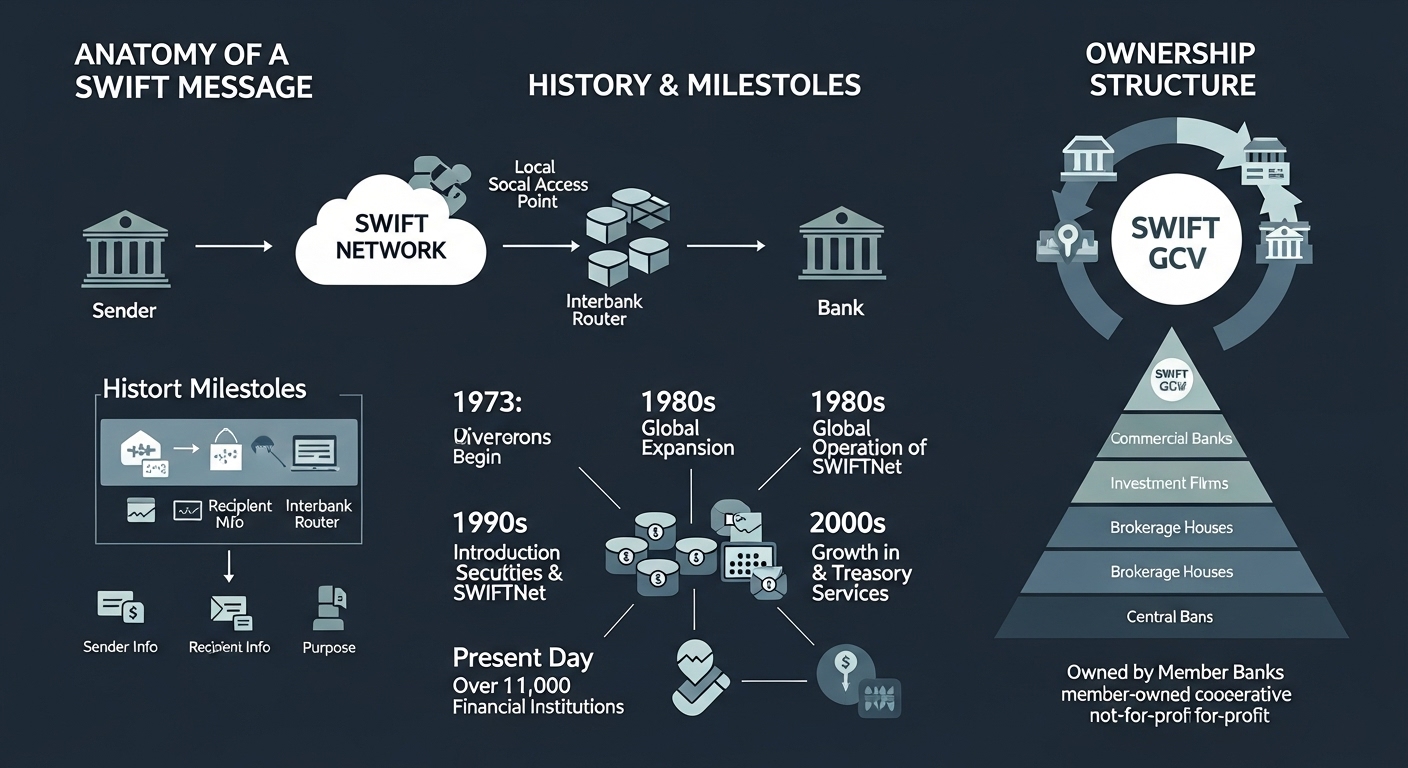

At its core, SWIFT is a messaging network, not a payment system that holds or transfers funds directly. Its primary function is to facilitate the secure and standardized exchange of payment instructions and other financial information between its member institutions. This distinction is crucial: money movement still occurs through correspondent banking relationships, but SWIFT provides the secure conduit for the instructions that initiate these transfers [1].

SWIFT Codes (BIC)

A fundamental component of the SWIFT system is the Bank Identifier Code (BIC), often referred to as a SWIFT code. Each financial institution connected to the network is assigned a unique 8- or 11-character code, which precisely identifies the bank, country, location, and optionally, a specific branch. For example, the code UNCRITMM for UniCredit Banca in Milan breaks down as follows:

| Component | Description | Example (UNCRITMM) |

| First four characters | Institute code (bank identifier) | UNCR |

| Next two characters | Country code (ISO 3166-1 alpha-2) | IT |

| Next two characters | Location code (city) | MM |

| Last three characters | Optional branch code (if applicable) | (Not applicable) |

When an international money transfer is initiated, the sender’s bank uses the recipient’s SWIFT/BIC code, along with account details, to send a payment message over the SWIFT network to the recipient’s bank. Upon receiving this secure message, the recipient’s bank processes and credits the funds to the designated account [1].

Core Services

SWIFT offers a range of services beyond basic payment messaging, continuously evolving to meet the complex demands of global finance. These include:

•Applications: Real-time instruction matching for treasury and forex transactions, banking market infrastructure for inter-bank payment processing, and securities market infrastructure for clearing and settlement instructions [1].

•Business Intelligence: Dashboards and reporting utilities that provide real-time monitoring of messages, activity, and trade flow, with filtering options by region, country, and message types [1].

•Compliance Services: Tools and reporting for financial crime compliance, including Know Your Customer (KYC), sanctions screening, and anti-money laundering (AML) solutions [1].

•Messaging, Connectivity, and Software Solutions: The core offering, providing a secure, reliable, and scalable network for transactional messages through various hubs, software, and network connections [1].

History of Origin

Before SWIFT, international financial communication heavily relied on the Telex system. Telex was slow, lacked standardized message formats, and presented significant security concerns, leading to frequent human errors and processing delays in international fund transfers [1].

The need for a more robust and efficient system became evident in the late 1960s. This led to the formation of SWIFT in 1973 by 239 banks across 15 countries. The cooperative utility was founded with a shared vision to transform cross-border value transfer, with its headquarters established in Belgium [2].

Key historical milestones include:

•1977: SWIFT’s messaging services officially went live, connecting 518 institutions from 22 countries. This marked a significant leap in efficiency, security, and reliability for international financial communications [2].

•1980s: The network expanded its global reach, with Hong Kong and Singapore commencing live operations. In 1983, central banks began connecting to SWIFT, solidifying its role within the financial industry. By the end of the decade, the community grew to over 2,800 institutions, handling nearly 300 million messages annually [2].

•1990s: A decade of innovation saw message volumes skyrocket, with the same amount of messages sent daily as previously annually. SWIFT was recognized with the Computerworld Smithsonian Information Technology Award in 1991 for its transformative impact. Interbank File Transfer went live, and the network achieved an industry-leading 99.98% FIN availability rate [2].

•2000s: SWIFT became the backbone of the global economy, processing billions of messages annually (3.76 billion messages per year between 9,000 institutions in 200 countries and territories). This era saw the introduction of SwiftNet, Innotribe, and the migration to ISO 15022 and ISO 20022 standards [2].

•2010s: The birth of SWIFT GPI (Global Payments Innovation) revolutionized cross-border payments by offering real-time tracking for transactions. The Customer Security Programme was launched to enhance cybersecurity and fraud protection. A phased global migration to ISO 20022 was announced, promising richer, more structured data for financial messaging [2].

•2020s: The ISO 20022 migration continues to progress, with successful live trials of digital currency and asset transactions. SWIFT is actively exploring the use of AI to detect anomalies and protect against fraud, aligning with the G20’s ambitious targets for enhancing speed, transparency, cost, and accessibility of cross-border payments by 2027 [2].

Ownership Structure

SWIFT operates as a member-owned cooperative under Belgian law. It is not controlled by any single commercial entity or government. Its ownership rests with its shareholders, which are financial institutions that are also members of the network [1, 3].

The governance of SWIFT is structured to ensure neutrality and represent the interests of its diverse global membership. Shareholders elect a Board of 25 Directors to oversee the organization’s operations [3].

Furthermore, SWIFT is subject to oversight by the Group of Ten (G-10) central banks. These countries include Belgium, Canada, France, Germany, Italy, Japan, Netherlands, Sweden, Switzerland, the United Kingdom, and the United States. Belgium, as the host country, acts as the lead overseer, working alongside other prominent central banks like the U.S. Federal Reserve [1]. This multi-national oversight reinforces SWIFT’s neutrality and its commitment to serving all its members equitably. The cooperative model ensures that the system is managed for the collective benefit of its participants, fostering trust and stability in the international financial system [1].

Conclusion

SWIFT has evolved from a visionary cooperative founded in 1973 into an indispensable global financial utility. Its robust messaging network, defined by standardized BIC codes and an expanding suite of services, underpins the vast majority of international financial transactions. Governed by its member institutions and overseen by G-10 central banks, SWIFT’s unique ownership structure reinforces its neutrality and commitment to secure, efficient, and reliable cross-border communication. As the financial landscape continues to digitize, SWIFT remains at the forefront, adapting to new technologies and challenges while upholding its foundational role in global commerce.

Be First to Comment