Executive Summary

This reference examines, in depth, what it takes to list a company on a public stock exchange across four of the world’s most significant capital markets — South Africa, the United States, Asia and London — and weighs the advantages and disadvantages of each.

The central finding is that beneath very different thresholds and cultures lies a common architecture. Every serious exchange tests an applicant on five dimensions: size and liquidity, financial track record, governance, disclosure, and the suitability of directors and controls. What differs is the calibration. The United States demands the most — quarterly reporting and the full weight of the Sarbanes-Oxley control regime — but rewards issuers with unrivalled liquidity and valuation. South Africa’s JSE provides a credible, well-regulated gateway to African capital, with the AltX board lowering the barrier for growing companies. Asia offers proximity to the fastest-growing economies and innovation-friendly listing chapters, at the cost of fragmentation and geopolitical risk. London, following its landmark 2024 listing reforms, has streamlined into a single commercial-company category and remains a leading international hub, with AIM among the world’s most successful growth markets.

The decision to list — and where — is therefore strategic rather than merely financial. It should align a company’s geography, sector, scale and ambition with the market best able to understand, value and sustain it.

[At a glance]

• South Africa (JSE): Africa’s gateway; Main Board and AltX; sponsor-supervised; IFRS; half-yearly reporting.

• United States (NYSE / Nasdaq): deepest liquidity; SEC + SOX; quarterly reporting; highest cost and litigation risk.

• Asia (HKEX, SGX, TSE, Mainland): China and ASEAN access; innovation chapters; fragmented across venues.

• London (LSE): international hub; single ESCC category since 2024; AIM for growth; comply-or-explain governance.

1 · Introduction and Purpose

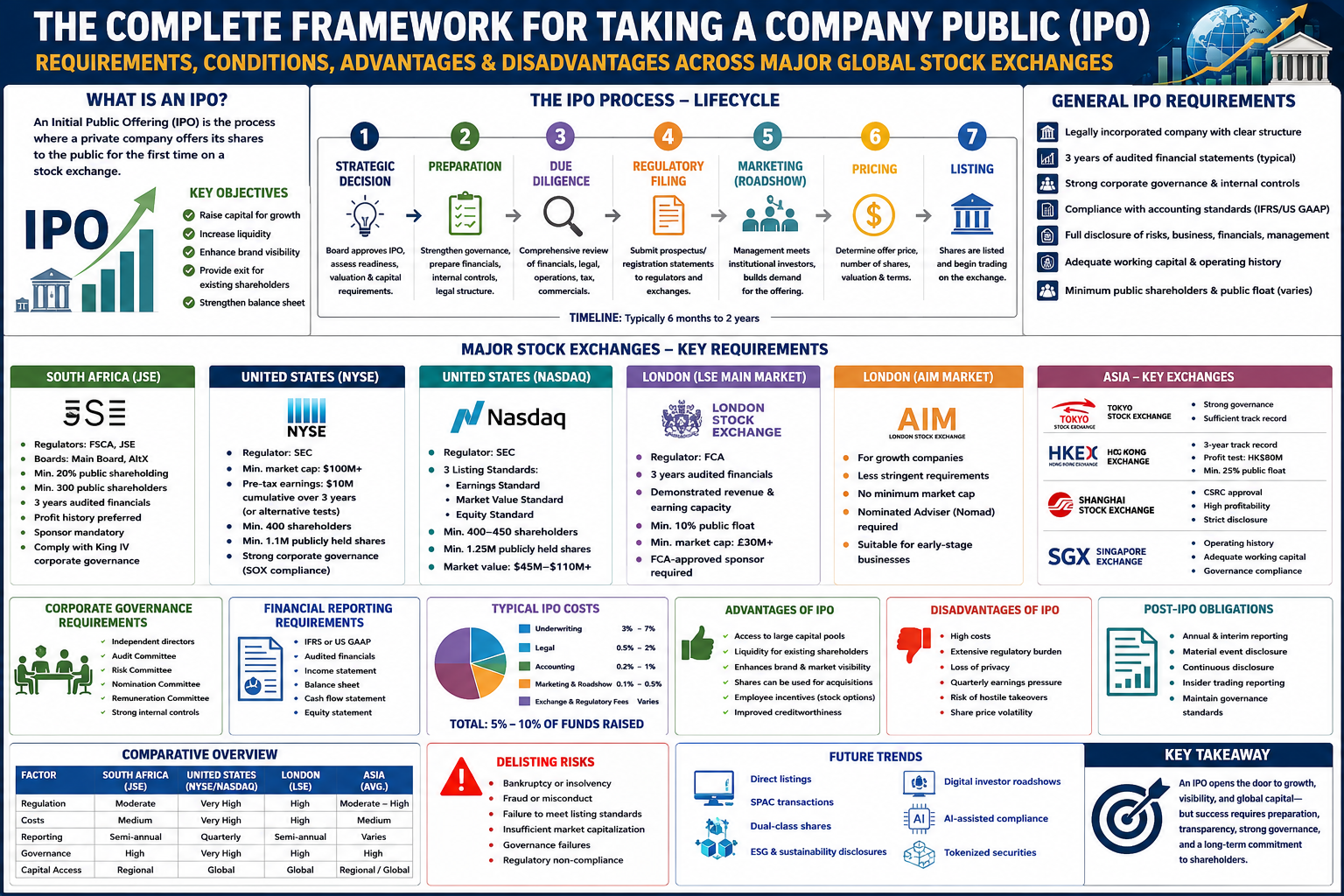

An Initial Public Offering (IPO) is the process by which a privately held company offers its shares to the public for the first time and secures admission to a recognised securities exchange. It is one of the most consequential events in a company’s life cycle: it converts a closely held enterprise into a publicly accountable entity, unlocks access to deep pools of capital, and subjects the company to a permanent regime of disclosure, governance and market scrutiny.

This document provides a comprehensive, comparative framework of the conditions and requirements for listing across four major jurisdictions: South Africa (the JSE), the United States (NYSE and Nasdaq), Asia (with emphasis on Hong Kong, Singapore, Tokyo and Greater China), and London (the LSE). For each, it sets out the regulatory architecture, the quantitative and qualitative eligibility criteria, the procedural pathway, and a balanced analysis of advantages and disadvantages.

[How to use this reference]

• Sections 2–3 establish the universal mechanics that apply in every market.

• Sections 4–7 examine each jurisdiction: regulator, tiers, thresholds, process and pros/cons.

• Sections 8–12 cover deal mechanics; 13–18 cover comparison, costs, pitfalls and market selection.

The intended audience is advanced. Listing requirements are amended frequently, so specific figures should always be confirmed against the current rulebooks of the relevant exchange and regulator, and professional counsel engaged before any listing decision.

2 · The Anatomy of a Public Listing

2.1 Primary versus secondary offerings

A listing can raise new money, sell existing shares, or both. In a primary offering the company issues new shares and the proceeds flow into the business. In a secondary offering existing shareholders sell their holdings, and the proceeds flow to them. Most IPOs combine both. A direct listing admits existing shares to trading without raising new capital at all.

2.2 The core participants

Participant | Role in the listing

Issuer | The company seeking to list; bears ultimate responsibility for the prospectus and disclosures.

Sponsor / Designated Adviser | A regulated firm that confirms the issuer’s suitability to the exchange (central in JSE and LSE regimes).

Underwriters / Bookrunners | Investment banks that structure, price, market and guarantee the offering.

Reporting Accountants / Auditors | Prepare and opine on historical financial information and working-capital statements.

Legal Advisers | Draft the prospectus, conduct due diligence, manage filings and verification.

Regulator | Reviews disclosure and approves the prospectus (SEC, FCA, FSCA, SFC, MAS).

Exchange | Sets and enforces listing rules and admits the securities to trading.

Registrar / Transfer Agent | Maintains the share register and processes settlement.

2.3 The universal building blocks of eligibility

Although thresholds differ widely, almost every exchange tests an applicant against the same five families of criteria:

• Size and liquidity — minimum market capitalisation, free float, number of public shareholders and value of shares in public hands.

• Financial track record — audited historical accounts, profit history, revenue or cash-flow tests, and a clean working-capital statement.

• Governance — board composition, independent directors, audit and remuneration committees, and adherence to a governance code.

• Disclosure — a prospectus or registration statement containing full, fair and accurate information, verified by advisers.

• Suitability and conduct — fit-and-proper directors, no disqualifying history, and adequate reporting and control systems.

3 · The Generic IPO Process and Timeline

Across all four jurisdictions the journey from private company to listed entity follows a broadly common sequence. The total elapsed time is typically six to eighteen months, depending on readiness, structural complexity and market conditions.

Phase 1 — Preparation and readiness (3–12 months before)

• Appoint advisers: sponsor/lead bank, lawyers, reporting accountants and a financial PR firm.

• Conduct an IPO-readiness assessment covering financials, controls, governance and the equity story.

• Restructure the group, settle related-party arrangements, and resolve tax and legal issues.

• Convert accounts to the required standard (IFRS or US GAAP) and build the mandated years of audited history.

Phase 2 — Due diligence and documentation (2–4 months)

• Perform legal, financial and commercial due diligence.

• Draft the prospectus / registration statement and verify every material statement.

• Prepare the working-capital report, long-form report and any competent-persons or valuation reports.

• File confidentially or publicly with the regulator and respond to comment letters.

Phase 3 — Marketing and pricing (2–6 weeks)

• Publish research (where permitted) and conduct an analyst presentation.

• Undertake a roadshow to institutional investors and build an order book (bookbuilding).

• Determine the price range, gather demand, and set the final offer price.

Phase 4 — Admission and aftermarket

• Allocate shares, admit the securities to trading and begin dealings on the first day.

• Stabilisation (greenshoe / over-allotment) may operate for up to 30 days.

• Lock-up periods restrict insider selling, typically for 90–365 days.

• Begin the permanent cycle of periodic and continuous disclosure.

[Continuing obligations never end]

Listing is not a destination but the start of a continuous regime: periodic reporting, immediate disclosure of price-sensitive information, restrictions on insider dealing, related-party controls, and annual governance reporting. Failure to comply can trigger suspension or delisting.

4 · South Africa — The Johannesburg Stock Exchange (JSE)

The JSE is the largest exchange in Africa and one of the oldest in the southern hemisphere, founded in 1887. It is a sophisticated, well-regulated market and the gateway to South African and broader African capital. Listings are governed by the JSE Listings Requirements, while prospectus issuance falls under the Companies Act, 2008 and the oversight of the Financial Sector Conduct Authority (FSCA).

4.1 Regulatory architecture

Body | Function

JSE Limited | Operates the exchange, writes and enforces the Listings Requirements, and admits securities.

FSCA | Market-conduct regulator overseeing fairness, disclosure and the Financial Markets Act.

CIPC | Companies and Intellectual Property Commission — registers prospectuses under the Companies Act.

King IV | Governance code applied on an “apply and explain” basis; mandatory for listed issuers.

4.2 The two main boards

Criterion | Main Board | AltX (growth board)

Subscribed capital (min.) | R50 million | R2 million

Profit history | 3-yr audited; R15m pre-tax in latest year (or alternative tests) | No formal profit requirement

Shares in public hands | At least 20% | At least 10%

Public shareholders (min.) | 300 | 100

Adviser required | Sponsor (JSE-approved) | Designated Adviser (DA)

Auditor status | JSE-accredited auditor | Accredited auditor

[Note on thresholds]

These figures reflect the broad standing requirements and are periodically revised. The Main Board offers alternative entry tests (subscribed capital, market capitalisation or revenue) for companies that do not meet the standard profit test. Always confirm against the current JSE Listings Requirements.

4.3 Advantages and disadvantages

Advantages:

• Access to the deepest pool of capital on the African continent and to emerging-market global investors.

• A highly regarded regulatory and settlement infrastructure that enhances credibility.

• AltX provides a genuine, lower-cost on-ramp for growing mid-market companies.

• Strong domestic institutional base of large pension and asset-management funds.

• Raised profile across Africa and a currency of listed shares for acquisitions.

Disadvantages:

• Low secondary-market liquidity outside the largest counters can depress valuations.

• Exposure to rand volatility and emerging-market risk premia widens the cost of capital.

• Concentrated institutional ownership can limit free-float depth for smaller issuers.

• Continuing-obligation and King IV reporting burden is heavy relative to company size on AltX.

• Vulnerability to global capital outflows during risk-off periods.

5 · The United States — NYSE and Nasdaq

The United States hosts the deepest, most liquid equity markets in the world. The NYSE is historically the home of large industrials and financials; Nasdaq is the electronic market favoured by technology and growth companies. Both operate under the federal securities laws administered by the Securities and Exchange Commission (SEC).

5.1 Regulatory architecture

Instrument / Body | Function

SEC | Federal regulator; reviews and declares the registration statement effective.

Securities Act 1933 | Governs the IPO itself and prospectus disclosure (S-1 / F-1).

Exchange Act 1934 | Governs continuous reporting and market conduct (10-K, 10-Q, 8-K).

Sarbanes-Oxley (SOX) | Mandates internal control over financial reporting (s.404) and CEO/CFO certification.

NYSE / Nasdaq | Set quantitative and qualitative listing standards and admit securities.

5.2 Quantitative listing standards (representative)

Criterion | NYSE | Nasdaq Global Select

Earnings test | Aggregate pre-tax income ≥ US$10m over 3 yrs | Aggregate pre-tax income ≥ US$11m over 3 yrs

Market value of public shares | ≥ US$40m (IPO) | ≥ US$45m (income standard)

Public shareholders | ≥ 400 holders of 100+ shares | ≥ 450 round-lot holders (or 2,200 total)

Publicly held shares | ≥ 1.1 million | ≥ 1.25 million

Minimum bid price | ≥ US$4.00 | ≥ US$4.00

Companies need satisfy only one applicable standard per exchange.

[Foreign private issuers and the JOBS Act]

Non-US companies can list as Foreign Private Issuers (FPIs) on Form F-1, with home-country governance accommodations. The JOBS Act created the “Emerging Growth Company” (EGC) category — issuers under roughly US$1.235bn in revenue — permitting confidential draft filings, only two years of audited financials in the prospectus, and a phase-in of certain SOX and compensation rules for up to five years.

5.3 Advantages and disadvantages

Advantages:

• Unmatched depth, liquidity and the largest concentration of institutional capital in the world.

• Premium valuations, especially for technology and high-growth companies on Nasdaq.

• Global visibility, analyst coverage and brand prestige.

• A highly developed ecosystem of underwriters, investors and analysts.

• Strong currency of stock for acquisitions and equity-based compensation.

Disadvantages:

• The highest compliance cost of any market: SOX s.404 alone can run into millions annually.

• Intense litigation risk — securities class actions are a structural feature.

• Demanding quarterly-earnings cadence encourages short-termism.

• Extensive, prescriptive disclosure and director-liability exposure.

• Severe delisting and reputational consequences if standards lapse.

6 · Asia — Hong Kong, Singapore, Tokyo and Greater China

Asia is not a single market but a constellation of major exchanges. The most internationally relevant venues are the Stock Exchange of Hong Kong (HKEX), the Singapore Exchange (SGX), the Tokyo Stock Exchange (TSE), and the Mainland markets in Shanghai and Shenzhen — including the STAR Market and ChiNext growth boards.

6.1 Hong Kong — HKEX

Hong Kong is the principal gateway between international capital and Mainland China. Listings are governed by the HKEX Listing Rules and overseen by the Securities and Futures Commission (SFC).

Main Board test (satisfy one) | Threshold (approx.)

Profit test | Aggregate profit ≥ HK$80m over 3 yrs (≥ HK$35m latest yr); market cap ≥ HK$500m

Market cap / revenue test | Market cap ≥ HK$4bn and revenue ≥ HK$500m latest yr

Market cap / revenue / cash-flow | Market cap ≥ HK$2bn, revenue ≥ HK$500m, operating cash flow ≥ HK$100m over 3 yrs

Public float | ≥ 25% of shares in public hands; minimum 300 shareholders

[Innovation-friendly chapters]

HKEX offers specialised regimes: Chapter 18A permits pre-revenue biotech listings; Chapter 18C accommodates “Specialist Technology Companies”; and the rules allow weighted-voting-rights (dual-class) structures and secondary listings for qualifying Greater China and international issuers.

6.2 Singapore — SGX

Singapore positions itself as a stable, well-governed hub for South-East Asia, REITs and family enterprises. SGX has a Mainboard and the sponsor-supervised Catalist growth board.

Mainboard test (satisfy one) | Threshold (approx.)

Profit test | Pre-tax profit ≥ S$30m cumulatively, or profitable latest yr with market cap ≥ S$150m

Market-cap test | Operating revenue latest yr and market cap ≥ S$300m

Public float | 12%–25% in public hands depending on market cap; ≥ 500 shareholders

6.3 Tokyo — TSE (Japan Exchange Group)

The TSE restructured into three segments in 2022 — Prime (large-cap, globally oriented, ≥ 35% tradable ratio), Standard (established domestic companies) and Growth (high-potential younger firms where business-plan disclosure is emphasised over current profit).

6.4 Mainland China — STAR Market and ChiNext

Shanghai and Shenzhen operate under the China Securities Regulatory Commission (CSRC). STAR (Shanghai) and ChiNext (Shenzhen) are registration-based growth boards for technology and innovation companies, offering multiple standards including unprofitable-but-high-growth tests. Access for foreign-controlled issuers is constrained, and capital controls are significant.

6.5 Advantages and disadvantages

Advantages:

• Direct access to the fastest-growing economies and a vast, increasingly wealthy investor base.

• Hong Kong bridges to Mainland Chinese capital and Stock Connect flows.

• Innovation-tailored regimes (biotech, specialist tech, dual-class) attract new-economy issuers.

• Premium valuations for companies with a credible Asian growth story.

• Singapore offers stability, rule-of-law certainty and a leading REIT framework.

Disadvantages:

• Fragmentation: each market has its own language, rules, investor culture and currency.

• Geopolitical and regulatory risk, particularly around Greater China and cross-border data.

• Mainland markets impose capital controls and restrictions on foreign-controlled issuers.

• Liquidity outside flagship counters can be thin on some boards.

• Currency, disclosure-language and local-adviser requirements raise execution complexity.

7 · London — The London Stock Exchange (LSE)

London is one of the world’s pre-eminent international financial centres. The LSE offers a two-tier structure: the Main Market (a regulated market) and AIM (a globally successful junior market for growth companies). The Financial Conduct Authority (FCA), as UK Listing Authority, maintains the Official List and the Listing Rules.

7.1 Regulatory architecture and the 2024 reform

In July 2024 the FCA implemented the most significant overhaul of the UK listing regime in decades. The previous “Premium” and “Standard” segments for commercial-company equity were replaced by a single category: Equity Shares (Commercial Companies), or ESCC. The reform removed certain mandatory shareholder votes and the historic three-year revenue track-record and clean-working-capital eligibility hurdles, shifting toward a more disclosure-based, investor-judgement model designed to make London more competitive.

Body / Instrument | Function

FCA (UK Listing Authority) | Maintains the Official List, approves prospectuses, writes the UK Listing Rules.

LSE | Operates the Main Market and AIM and admits securities to trading.

UK Listing Rules (2024) | Single ESCC category replacing Premium/Standard for commercial-company equity.

UK Corporate Governance Code | Applies on a “comply or explain” basis to ESCC issuers.

Nominated Adviser (Nomad) | Mandatory adviser that vouches for AIM applicants and supervises them continuously.

7.2 Main Market (ESCC) requirements

• A prospectus approved by the FCA under the UK Prospectus Regulation.

• Expected market value of at least £30 million for listed equity shares.

• At least 10% of shares in public hands (free float).

• Audited historical financial information (IFRS or equivalent), even though the three-year-track-record eligibility hurdle was removed in 2024.

• Compliance with the UK Corporate Governance Code on a comply-or-explain basis.

• Eligible shares freely transferable and capable of electronic settlement (CREST).

7.3 AIM requirements

AIM has no minimum market-cap, free-float or trading-record requirement; suitability is policed by the Nominated Adviser.

• A Nomad must be appointed at admission and retained at all times — losing the Nomad triggers suspension.

• An admission document (lighter than a full prospectus where no public offer is made).

• A broker must be appointed to support liquidity.

• No minimum free float, profit history or market-cap threshold is prescribed.

• Compliance with the AIM Rules and a recognised governance code (e.g. QCA Code).

7.4 Advantages and disadvantages

Advantages:

• A leading international centre with a deep base of global institutional investors.

• AIM is one of the world’s most successful growth markets, with a flexible, adviser-led regime.

• The 2024 reforms reduced friction and made the Main Market more accessible.

• English law and a time-zone bridge between Asia and the Americas.

• Strong appetite for international, resources, financial and dual-listed issuers.

Disadvantages:

• London valuations and liquidity have lagged US markets for high-growth tech.

• AIM companies can suffer thin liquidity and high volatility.

• Post-Brexit divergence from EU rules adds cross-border complexity.

• Continuing-obligation and governance reporting remain demanding for smaller issuers.

• A perception of capital migration to New York has pressured some issuers.

8 · Due Diligence and the Prospectus

Due diligence is the investigative spine of every IPO. Its purpose is twofold: to verify that the prospectus is true, complete and not misleading, and to protect directors and advisers from liability for any material misstatement or omission. Because directors and, in many jurisdictions, the underwriters and experts carry statutory and common-law liability, the rigour of due diligence is not a formality but a defence.

8.1 The three streams

Financial due diligence

Reporting accountants examine historical information, quality of earnings, working-capital adequacy and forecasts. The working-capital statement — a director-level confirmation of sufficient working capital for at least twelve months — is a cornerstone of UK, JSE and Hong Kong practice and demands a detailed cash-flow model stress-tested against downside scenarios.

Legal due diligence

Legal advisers verify corporate structure, title to assets, material contracts, litigation, IP, employment, licences, real estate and tax. Every material statement is traced to documentary evidence through verification — the notes become a permanent liability-defence record.

Commercial due diligence

Often supported by an independent market report, this tests market position, competitive landscape, addressable market, customer concentration and the plausibility of the growth narrative underpinning the valuation.

8.2 Anatomy of the prospectus

Section | Content

Summary | Concise overview of the company, the offer and key risks.

Risk factors | Comprehensive, specific risks to the business, industry and securities.

Business description | Strategy, products, markets, operations and competitive position.

Financial information | Audited historical accounts, MD&A / operating review, and capitalisation.

Management & governance | Directors, senior management, board structure, committees, remuneration.

Use of proceeds | How the new capital will be deployed.

Details of the offer | Structure, pricing, dilution, lock-ups and settlement.

Additional / statutory | Material contracts, related-party transactions, legal proceedings, share capital.

[Liability for the prospectus]

In every jurisdiction studied, directors accept responsibility for the document and confirm — in a formal responsibility statement — that the information accords with the facts and contains no material omission. Misstatements can attract civil liability, regulatory sanction and, in egregious cases, criminal exposure. This is why verification is exhaustive.

9 · Valuation, Pricing and Allocation Mechanics

Setting the offer price is part science, part market judgement. Price too high and the offer breaks in the aftermarket; price too low and the company leaves money on the table through excessive underpricing. The aim is a clearing level that rewards new investors with a modest first-day gain while maximising proceeds and building a stable shareholder base.

9.1 Common valuation methods

• Comparable companies — benchmarking trading multiples (P/E, EV/EBITDA, EV/Revenue) of listed peers.

• Precedent transactions — multiples implied by recent M&A in the sector.

• Discounted cash flow (DCF) — intrinsic valuation of projected free cash flows.

• Sum-of-the-parts — valuing distinct divisions separately for diversified groups.

9.2 Pricing mechanisms

Mechanism | How it works

Bookbuilding | Underwriters market a range, collect institutional demand and set the price from the book. The global standard.

Fixed price | The price is set in advance; investors subscribe at that price. Common for smaller, retail-heavy offers.

Auction (Dutch) | Investors bid price and quantity; a clearing price is derived.

Direct listing | Existing shares are admitted with no new issue and no set price; the market opens via a reference price.

9.3 Stabilisation and the greenshoe

Underwriters are typically granted an over-allotment (greenshoe) option of up to around 15%. By over-allocating and buying back if the price falls — or exercising the option if it rises — the stabilising manager can support the price for a limited window, usually up to thirty days after admission.

9.4 Lock-ups and the free float

Lock-up agreements restrain founders, directors and pre-IPO investors from selling for a defined period (commonly 180 days; 90–365 days are all seen) to prevent an early flood of supply. The free float must be large enough to support orderly trading; an inadequate float is both a liquidity problem and, in most markets, a breach of the listing rules.

10 · Continuing Obligations of a Listed Company

Admission marks the beginning, not the end, of regulatory responsibility. The continuing-obligations regime is broadly comparable across jurisdictions, differing mainly in cadence and prescriptive detail.

10.1 Periodic financial reporting

Market | Reporting cadence

United States | Annual (10-K) and quarterly (10-Q), plus current reports (8-K) on material events.

South Africa (JSE) | Audited annual statements and reviewed interim (half-yearly) results.

Hong Kong / Singapore | Annual report plus half-yearly (historically quarterly for some boards) results.

London (LSE) | Annual report and half-yearly report under the Disclosure and Transparency Rules.

10.2 Continuous disclosure of inside information

Every market imposes a duty to disclose price-sensitive information promptly and without selective disclosure — embodied in US Regulation FD, the UK/EU Market Abuse Regulation, and equivalent JSE and Asian rules. Selective leakage, delay or insider dealing attracts severe penalties.

10.3 Governance and shareholder protections

• Maintaining required board independence and functioning audit, remuneration and nomination committees.

• Annual governance reporting against the applicable code (King IV, UK Code, exchange codes).

• Shareholder approval for significant or related-party transactions above thresholds.

• Restrictions on dealings by directors and PDMRs, with closed periods around results.

• Equal treatment of shareholders and controls over new-share issuance and pre-emption rights.

10.4 Consequences of non-compliance

Breaches can lead to censure, fines, suspension and ultimately delisting. Beyond formal sanctions, the reputational damage of a suspension or restatement can permanently impair access to capital and investor confidence.

[The cultural shift of being public]

The most underestimated consequence of listing is cultural. A public company operates in a glass house: its results, governance and missteps are visible and consequential. Management must communicate consistently with the market, plan around disclosure calendars, and accept that strategic decisions will be judged in real time.

11 · Dual Listings, Secondary Listings and Cross-Border Structures

Larger, internationally minded issuers frequently pursue dual or secondary listings to broaden their investor base, deepen liquidity, gain multi-market index inclusion, or hedge single-venue risk. South African companies have a long history of inward and dual listings on the JSE alongside London.

11.1 Types of multi-market listing

Structure | Description

Primary dual listing | Full primary listings on two exchanges, complying with both rulebooks.

Secondary listing | A primary home listing with a lighter-touch secondary listing elsewhere.

Inward listing | A foreign company lists on a local exchange (e.g. inward-listing on the JSE).

Depositary receipts | ADRs (US) or GDRs (London/Luxembourg) representing home-market shares.

Fast-track / Stock Connect | Streamlined routes such as HKEX secondary listings and China–Hong Kong Connect.

11.2 Why companies dual-list

• Access to a larger, more diverse pool of capital across time zones.

• Improved liquidity and the potential for a higher overall valuation.

• Index inclusion in multiple markets, drawing passive flows.

• Currency diversification and a natural hedge for multinational operations.

• Enhanced profile and credibility in strategic markets.

11.3 The costs and complications

• Compliance with two (sometimes conflicting) sets of rules and governance codes.

• Duplicated reporting, audit and adviser costs.

• Liquidity fragmentation across venues.

• Arbitrage and price-discrepancy management between the two lines of stock.

• Complex tax, settlement and FX-control considerations for emerging-market issuers.

[Depositary receipts in brief]

A depositary receipt is a negotiable certificate issued by a bank representing shares in a foreign company, letting investors hold foreign equity in their home market and currency. ADRs serve US investors; GDRs serve international investors via London or Luxembourg. They are a lighter alternative to a full secondary listing.

12 · Alternatives and Adjacent Routes to Going Public

A traditional underwritten IPO is the best-known route but not the only one. Depending on objectives, scale and capital needs, several alternatives may be more appropriate.

Route | Essence | Best suited to

Traditional IPO | Underwritten primary/secondary offer with bookbuilt pricing. | Companies needing capital and a broad investor base.

Direct listing | Existing shares admitted without raising new capital or underwriting. | Well-known, cash-rich companies seeking liquidity.

SPAC merger | Merger with a listed special-purpose acquisition shell. | Companies seeking speed and price certainty (with dilution).

Reverse takeover | A private company acquires control of a listed shell. | Companies seeking a listing without a full new offer.

Introduction | Admission of already-dispersed shares with no offer. | Companies whose shares are already widely held.

Each route carries trade-offs. SPACs offer speed and negotiated pricing but can be dilutive and face heightened scrutiny. Direct listings avoid underwriting fees but raise no new money in their classic form. Reverse takeovers can be quicker and cheaper but carry shell-legacy risk and still trigger re-admission requirements.

[The capital-raising question first]

Before selecting any route, answer one question precisely: do we primarily need new capital, liquidity for existing holders, an acquisition currency, or simply a public profile? An IPO solves all four; a direct listing solves liquidity and profile but not capital; a SPAC can solve capital and speed at the cost of dilution.

13 · Comparative Analysis Across the Four Jurisdictions

Feature | JSE (SA) | NYSE / Nasdaq (US) | HKEX (Asia) | LSE (London)

Primary regulator | JSE + FSCA | SEC | SFC | FCA

Senior board | Main Board | NYSE / Nasdaq | Main Board | Main Market (ESCC)

Growth board | AltX | Nasdaq tiers | GEM | AIM

Adviser gatekeeper | Sponsor | Underwriters | Sponsor | Nomad (AIM)

Accounting standard | IFRS | US GAAP / IFRS (FPI) | IFRS / HKFRS | IFRS

Min. free float | 20% (Main) | Holder/share tests | 25% | 10%

Track-record rule | 3-yr profit (Main) | Multiple tests | 3-yr profit/size | Removed (2024)

Reporting cadence | Half-yearly | Quarterly | Half-yearly | Half-yearly

Signature strength | Africa gateway | Liquidity & valuation | China gateway | International hub

[A key structural difference: reporting cadence]

The United States is distinctive in requiring full quarterly reporting (10-Q). South Africa, Hong Kong, Singapore and London generally require half-yearly reporting plus continuous disclosure of price-sensitive information. This single difference materially shapes management’s time horizon and the cost of being public.

14 · The Cost of Going and Being Public

IPO expense falls into one-off transaction costs to achieve the listing and recurring costs of remaining public. These vary by market, deal size and complexity, but the structure is universal.

14.1 One-off costs of the offering

Cost item | Typical basis

Underwriting / placing commission | Usually the largest single cost; commonly 2%–7% of gross proceeds (highest in the US).

Legal fees | Issuer’s and underwriters’ counsel; scales with complexity and jurisdictions.

Reporting accountants / audit | Historical financials, working-capital and long-form reports.

Exchange & regulator fees | Initial listing and prospectus-review fees.

Financial PR & roadshow | Investor relations, printing, marketing and logistics.

Sponsor / Nomad / adviser fees | Fixed and success-based components.

14.2 Recurring costs of being listed

• Enhanced audit and internal-control costs (markedly higher under SOX in the US).

• Annual listing fees, registrar fees and ongoing adviser/Nomad retainers.

• Investor-relations function, periodic-reporting production and AGM costs.

• Directors’ and officers’ (D&O) liability insurance, far higher for US issuers.

• Additional governance, compliance and company-secretarial headcount.

15 · Common Pitfalls and Readiness Failures

A large proportion of aborted or underperforming IPOs fail for predictable, avoidable reasons:

• Inadequate financial systems — inability to close the books quickly and accurately to a public-company standard.

• Weak internal controls — material weaknesses surfaced during due diligence (especially SOX scoping).

• Governance immaturity — boards lacking sufficient independent directors or functioning audit committees.

• An unconvincing equity story — poorly articulated growth narrative and unrealistic forecasts.

• Unresolved related-party arrangements — founder loans and intra-group conflicts must be cleansed first.

• Poor market timing — launching into hostile or volatile windows leads to pulled deals.

• Tax and structural complexity — an unsuitable holding structure can stall the process.

• Inadequate free float — over-allocation to insiders impairs aftermarket liquidity and can breach rules.

[The readiness mindset]

Successful issuers begin behaving like public companies twelve to twenty-four months before admission: tightening the financial close, building the board, formalising controls and rehearsing disclosure. The IPO then confirms readiness rather than scrambling to achieve it.

16 · Choosing the Right Market

There is no universally superior exchange; the optimal venue depends on geography, sector, scale, investor base and ambition.

16.1 Decision factors

• Where is your story understood? List where investors know your sector and customers.

• What is your scale? Smaller companies suit AltX, AIM, Catalist or GEM over senior US boards.

• What is your sector? High-growth tech often achieves premium valuations on Nasdaq or HKEX’s tech chapters; resources and financials suit London and Johannesburg.

• What governance burden can you bear? The US imposes the heaviest load.

• Do you need acquisition currency or employee equity? Deep, liquid markets make stock more useful.

16.2 Typical archetypes

Company archetype | Often best suited to

African mid-market growth company | JSE AltX, then JSE Main Board

Global high-growth technology firm | Nasdaq (US) or HKEX Chapter 18C

Company seeking Mainland China capital | HKEX Main Board

South-East Asian REIT or family enterprise | SGX Mainboard / Catalist

International resources or financial issuer | LSE Main Market

Smaller UK/European growth company | LSE AIM

17 · Conclusion

Listing on a public stock exchange remains one of the most powerful instruments for raising capital, creating shareholder liquidity, and elevating a company’s standing. Yet it is also a profound and permanent change of state. The privileges of public capital are inseparable from the obligations of public accountability: full disclosure, robust governance, and the discipline of the market’s continuous judgement.

Across South Africa, the United States, Asia and London, the underlying architecture is strikingly consistent — size, track record, governance, disclosure and suitability — even as thresholds, costs and cultural expectations diverge sharply. The JSE offers the gateway to African capital with a credible regulatory backbone. The United States offers unrivalled liquidity and valuation at the price of the world’s most exacting compliance regime. Asia offers proximity to the fastest-growing economies and innovation-friendly chapters, at the cost of fragmentation and geopolitical risk. London offers an international hub whose 2024 reforms have meaningfully lowered the barrier to entry.

The decision to list, and where, should be taken not as a financing event in isolation but as a long-term strategic commitment — one that aligns the company’s geography, sector, scale and ambition with the market best able to understand, value and sustain it over the years that follow admission.

18 · Glossary of Key Terms

Term | Meaning

Free float | The proportion of shares held by the public and freely tradable, excluding locked-in insiders.

Bookbuilding | Gathering investor demand at various prices to set the final offer price.

Greenshoe | An over-allotment option allowing underwriters to stabilise the price post-listing.

Lock-up | A period after listing during which insiders are restricted from selling shares.

Sponsor / Nomad / DA | A regulated adviser confirming an applicant’s suitability and supervising it (JSE, LSE-AIM, SGX).

Prospectus | The principal legal disclosure document offering securities to the public.

FPI | Foreign Private Issuer — a non-US company listing in the US with certain accommodations.

EGC | Emerging Growth Company — a US JOBS Act category with scaled disclosure relief.

ESCC | Equity Shares (Commercial Companies) — the UK’s single listing category introduced in 2024.

SOX | The US Sarbanes-Oxley Act governing internal control over financial reporting.

Be First to Comment